Reporting in the case of notional cash pooling

- Question ID: 2020/0015

- Date of publication: 31/01/2020

- Subject matter: Cash pooling

Question

Please clarify the reporting of cash pooling under AnaCredit on the basis of the following stylised example. A group, consisting of Company A (the parent company), Company B and Company C, signed a cash-pool agreement in February. According to the contract, the cash pool is operated by Bank X, and receivables and payables are exclusively settled internally, where an agreed interest rate on outstanding balances is payable by companies owing to companies lending. In addition, the bank and the group agree on a credit facility in the form of a line of credit in an amount of up to €10 million committed by the bank. The credit facility money can be drawn by the individual companies whenever a need for liquidity arises. All the entities are liable vis-à-vis the bank only to the extent to which they utilise the bank’s funds (drawn via their own individual accounts). The outstanding principal balance of the credit facility bears interest at the contract rate of 4.5% per annum. Once the amounts advanced under the credit facility are repaid, they may be re-advanced insofar as the aggregate amount of outstanding advances on the credit facility does not exceed the committed credit line.

Answer

Please refer to Q&A Cash pooling under AnaCredit for general guidance on reporting to AnaCredit in the case of cash pooling.

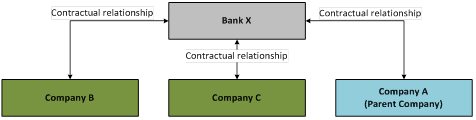

The situation presented in the example corresponds to an instance of notional cash pooling. The following chart illustrates the contractual relationship between the bank and the cash pool participants.

Figure 1 Contractual relationship between the bank and the cash pool participants

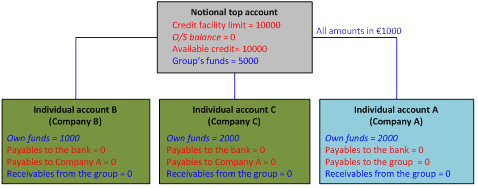

At the end of February the group’s own funds amount to €9 million and are sufficient to cover the group’s outstanding monetary obligations (of €4 million). In this situation, the group does not utilise the credit facility. Figure 2 depicts the situation immediately after the group has paid its obligations.

Figure 2 The group’s payables and receivables and the notional top account as at February

This structure is reported to AnaCredit since the bank participates as a creditor in the arrangement (where the debtors are allowed to draw funds made available to them via overdraft accounts). The following tables present the reporting to AnaCredit as at the end of February.

With regard to reportable instruments, as the group’s entities are enabled to draw the bank’s funds via the individual company’s accounts and have a direct contractual relationship with the bank, each of the individual instances of credit meets the definition of instrument in AnaCredit and is subject to AnaCredit reporting. Meanwhile, the notional top account – which only consolidates the funds of the group on a fictitious basis – is not subject to AnaCredit reporting.

Table 1Indication of the instrument dataset for the cash-pool accounts

Reporting reference date |

Contract identifier |

Instrument identifier |

Type of instrument |

Inception date |

28/02/2019 |

Cshpl#1 |

InDVDLACCNT#B |

Overdrafts |

15/02/2019 |

28/02/2019 |

Cshpl#1 |

InDVDLACCNT#C |

Overdrafts |

15/02/2019 |

28/02/2019 |

Cshpl#1 |

InDVDLACCNT#A |

Overdrafts |

15/02/2019 |

For each individual account, the holder of the account is the only debtor vis-à-vis the bank (see Table 3). However, as the funds made available by the bank may be utilised by any entity of the group participating in the cash pool, the financing constitutes a multi-debtor credit cross-limit structure, which determines the off-balance-sheet amount available through the individual accounts connected in a system. By definition, the off-balance-sheet amount is the difference between the bank’s credit limit and the outstanding credit extended by the bank. In this case, since the group only utilises its own funds, no bank financing is used, implying that the group still has at its disposal the total credit (i.e. an off-balance-sheet amount vis-à-vis the bank of €10 million), which can be drawn by all the participants.

Note that for the purpose of reporting, the reporting agent (the bank) is assumed to allocate the notional top account’s off-balance-sheet amount of €10 million (as well as the commitment amount at inception) equally across the individual accounts (see the information on the reporting of credit cross-limits in Part III of the AnaCredit Reporting Manual).

Table 2Indication of the financial dataset for the cash-pool accounts

Reporting reference date |

Contract identifier |

Instrument identifier |

Interest rate |

Outstanding nominal amount |

Off-balance-sheet amount |

28/02/2019 |

Cshpl#1 |

InDVDLACCNT#B |

0.045 |

0.00 |

3,333,333.33 |

28/02/2019 |

Cshpl#1 |

InDVDLACCNT#C |

0.045 |

0.00 |

3,333,333.33 |

28/02/2019 |

Cshpl#1 |

InDVDLACCNT#A |

0.045 |

0.00 |

3,333,333.34 |

Table 3Indication of the counterparty-instrument dataset for the cash-pool accounts

Reporting reference date |

Contract identifier |

Instrument identifier |

Counterparty identifier |

Counterparty role |

28/02/2019 |

CSHPL#1 |

InDVDLACCNT#B |

Bank X |

Creditor |

28/02/2019 |

CSHPL#1 |

InDVDLACCNT#B |

Bank X |

Servicer |

28/02/2019 |

CSHPL#1 |

InDVDLACCNT#B |

company B |

Debtor |

28/02/2019 |

CSHPL#1 |

InDVDLACCNT#C |

Bank X |

Creditor |

28/02/2019 |

CSHPL#1 |

InDVDLACCNT#C |

Bank X |

Servicer |

28/02/2019 |

CSHPL#1 |

InDVDLACCNT#C |

company C |

Debtor |

28/02/2019 |

CSHPL#1 |

InDVDLACCNT#A |

Bank X |

Creditor |

28/02/2019 |

CSHPL#1 |

InDVDLACCNT#A |

Bank X |

Servicer |

28/02/2019 |

CSHPL#1 |

InDVDLACCNT#A |

company A |

Debtor |

Furthermore, as the group has its own funds in the cash pool, these are considered to serve as protection for the credit facility. This is reflected in the instrument-protection received dataset.

Table 4Indication of instrument-protection received dataset for the cash-pool

Reporting reference date |

Contract identifier |

Instrument identifier |

Protection identifier |

Protection allocated value |

28/02/2019 |

CSHPL#1 |

InDVDLACCNT#B |

COLL#B |

1,000,000 |

28/02/2019 |

CSHPL#1 |

InDVDLACCNT#C |

coLL#C |

2,000,000 |

28/02/2019 |

CSHPL#1 |

InDVDLACCNT#A |

COLL#A |

2,000,000 |

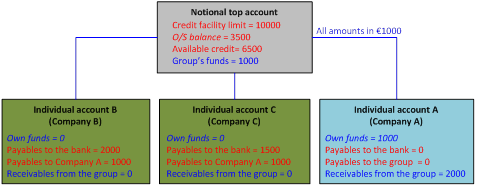

In the course of March the group accumulates own funds of €6 million and incurs obligations of €8.5 million that are due at the end of March. In this case, the obligations exceed the group’s own funds (by €2.5 million) and a need for liquidity arises on 31 March. Consequently, in order to meet the obligations, the bank’s funds (drawn via the companies’ individual accounts) are utilised. In this situation, benefiting from the cash pool, the bank settles the individual companies’ obligations so that any free cash above €1 million available within the group is utilised before the (more expensive) bank’s financing is drawn down. Figure 3 depicts this situation immediately after the obligations have been settled.

Figure 3 Group’s payables and receivables and the notional top account as at March

In this case, since the group first utilises its own funds of €5 million (and still keeps €1 million aside), the bank’s funds of €3.5 million are used to pay for the group’s monetary obligations (of €8.5 million). This also means that there is an off-balance-sheet amount vis-à-vis the bank of €6.5 million available to all the group’s entities.

Furthermore, if, for example, the reporting agent (the bank) allocates the notional top account’s off-balance-sheet amount of €6.5 million equally across the individual accounts, the three instruments are reported to AnaCredit as follows (the instrument and the counterparty-instrument datasets from February remain unchanged in this case).

Table 5Indication of the financial dataset for the cash-pool accounts

Reporting reference date |

Contract identifier |

Instrument identifier |

Interest rate |

Outstanding nominal amount |

Off-balance-sheet amount |

31/03/2019 |

Cshpl#1 |

InDVDLACCNT#B |

0.045 |

2,000,000 |

2,166,666.67 |

31/03/2019 |

Cshpl#1 |

InDVDLACCNT#C |

0.045 |

1,500,000 |

2,166,666.67 |

31/03/2019 |

Cshpl#1 |

InDVDLACCNT#A |

0.045 |

0 |

2,166,666.67 |

It should be noted that, although in this case the financing extended to companies B and C is a mixture of the bank’s as well as the group’s funds, only the credit extended by the bank consists of reportable instruments and is subject to AnaCredit reporting.

With regard to protection securing the bank’s financing, the cash of €1 million held by Company A only serves as protection in this situation. For the purpose of reporting, the bank allocates the amount to the instruments of Company B and C in proportion to the outstanding nominal amount (see Table 6 below)

Table 6Indication of instrument-protection received dataset as at March

Reporting reference date |

Contract identifier |

Instrument identifier |

Protection identifier |

Protection allocated value |

31/03/2019 |

CSHPL#1 |

InDVDLACCNT#B |

COLL#A |

571,428.57 |

31/03/2019 |

CSHPL#1 |

InDVDLACCNT#C |

COLL#A |

428,571.43 |

This virtual/notional top account determines the net pool position and represents the basis for calculating interest to be paid by or charged to the bank that operates the cash pool. This interest is then distributed among participants in accordance with the conditions specified by the agreement concluded by the members of the pool.

It should also be noted that the currency and the interest rate to be reported are the values pertaining to the individual accounts irrespective of the currencies or interest rates applied in the notional top account (although, in the example, the currency is the same and the participants agreed a single interest rate).

Related questions

See also Cash pooling under AnaCredit