The decrease in euro area net financial outflows in 2018: foreign direct investment retrenchment and portfolio investment slowdown

Published as part of the ECB Economic Bulletin, Issue 4/2019.

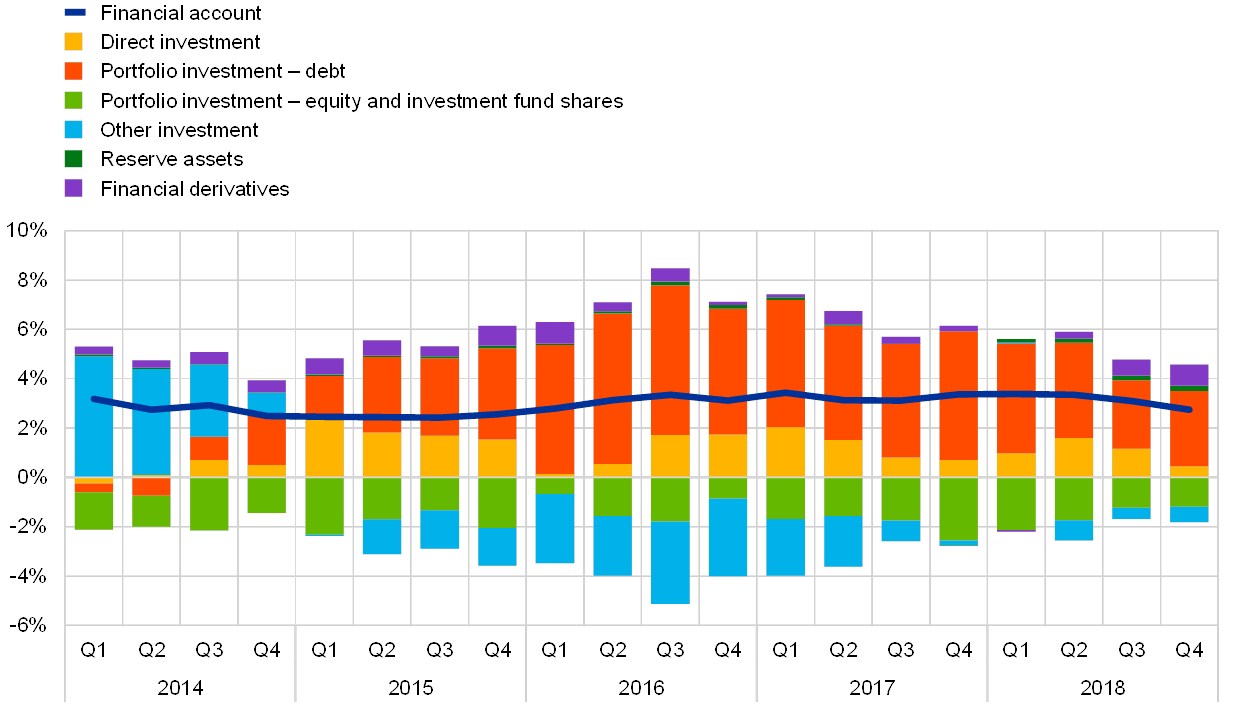

In 2018 the financial account of the euro area balance of payments recorded net outflows of 2.7% of euro area GDP (see Chart A). The decrease in net financial outflows, from 3.4% of GDP in 2017, is in line with the narrowing of the euro area current account surplus recorded in 2018 and partly reflects the stepwise reduction in the net purchases of the Eurosystem’s asset purchase programme (APP). The net outflows continued to be driven by portfolio investment in debt securities as well as – to a lesser extent – financial derivatives, foreign direct investment (FDI) and reserve assets. At the same time, the euro area recorded net inflows of portfolio investment in equity and other investment (largely comprising currency, loans and deposits).

Chart A

Main items of the euro area financial account

(four-quarter moving sums, percentages of GDP)

Sources: ECB and Eurostat.

Notes: A positive (negative) number indicates net outflows (inflows) from (into) the euro area. The latest observation is for the fourth quarter of 2018.

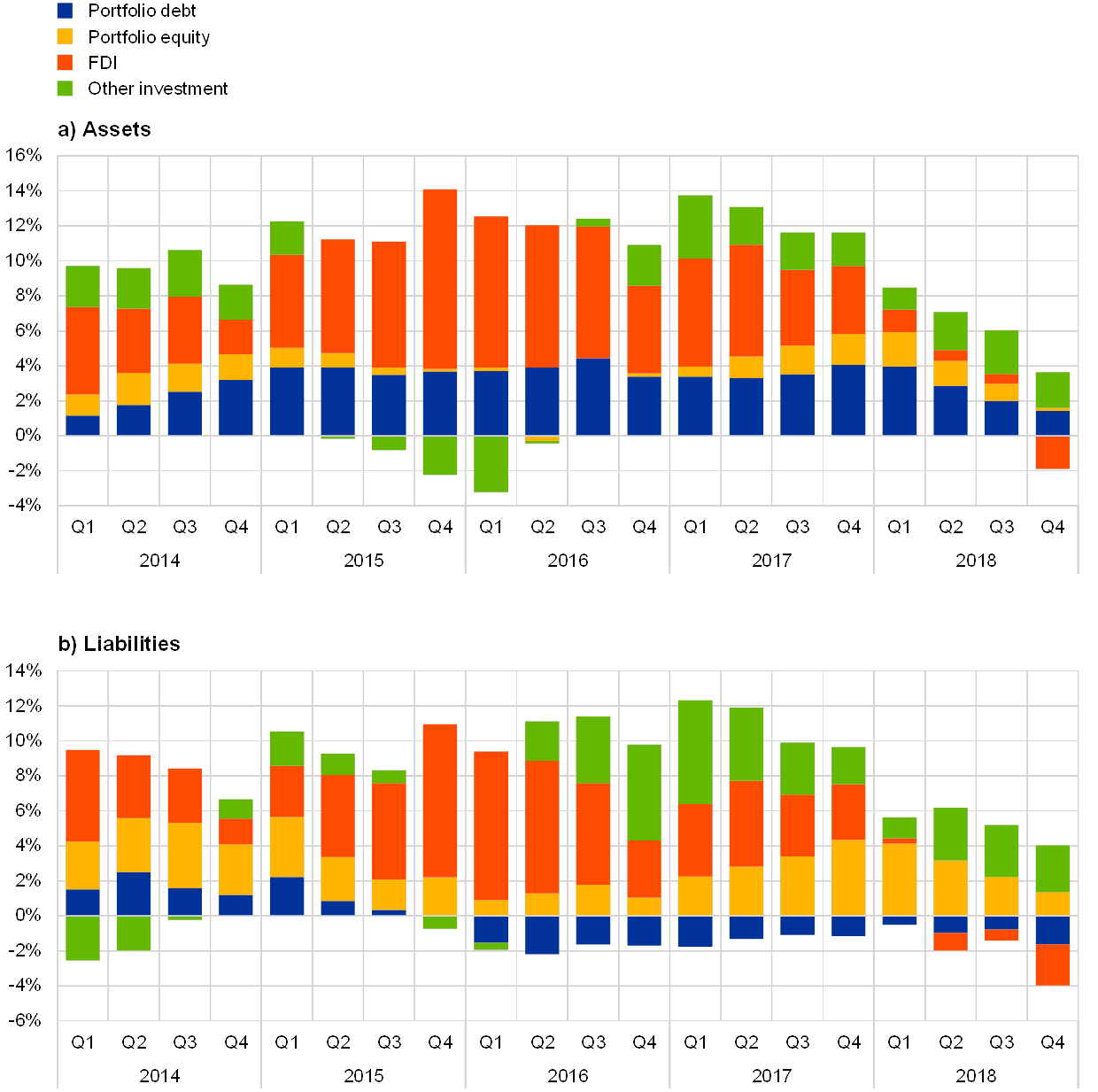

The decrease in the financial account balance coincided with a broad-based decline in cross-border financial flows in 2018 (see Chart B). On the assets side, euro area residents’ net purchases of non-euro area portfolio debt securities more than halved in 2018, falling to 1.4% of GDP from 4.1% of GDP in 2017, while net purchases of non-euro area portfolio equity decreased to 0.2% of GDP (from 1.8% of GDP in 2017). The largest change was recorded in FDI, as euro area residents made net disinvestments of 1.9% of GDP outside the euro area (compared with net investments of 3.9% of GDP in 2017). A similar development was also observed on the liabilities side, with non-residents making net disinvestments of 2.4% of euro area GDP (following net investments of 3.2% of GDP in the previous year). Moreover, non-euro area investors slightly increased their net sales of euro area portfolio debt securities to 1.6% of GDP, while their net purchases of euro area portfolio equity declined to 1.4% of GDP (from 4.3% of GDP in 2017).[1] The declines in euro area portfolio investment and FDI transactions in 2018 are broadly in line with those observed for other advanced economies.[2]

Chart B

Selected items of the euro area financial account

(four-quarter moving sums, percentages of GDP)

Sources: ECB and Eurostat.

Notes: For assets, a positive (negative) number indicates net purchases (sales) of non-euro area instruments by euro area investors. For liabilities, a positive (negative) number indicates net purchases (sales) of euro area instruments by non-euro area investors. The latest observation is for the fourth quarter of 2018.

Portfolio investment in non-euro area assets, particularly debt securities, continued to reflect the impact of the Eurosystem’s asset purchase programme in 2018.[3] Since the launch of the expanded APP in the first quarter of 2015, euro area residents have made persistent net purchases of foreign long-term debt securities in the light of the euro area’s negative interest rate differentials vis-à-vis other advanced economies (see Chart B). In particular, they have rebalanced their portfolios towards sovereign bonds issued by other advanced economies, most notably US Treasuries, as these serve as the closest substitute for securities eligible under the public sector purchase programme. At the same time, they also continued to be net buyers of foreign equity.[4] In 2018 euro area investors’ net purchases of US debt securities continued, while net acquisitions of debt securities issued by residents of Japan and the United Kingdom largely ceased, thereby contributing to an overall decline in net purchases of non-euro area debt securities. As in previous years, “financial corporations other than monetary financial institutions (MFIs)” – which include investment and pension funds, as well as insurance companies – accounted for the largest part of the euro area’s net purchases of foreign portfolio debt securities in 2018, followed by MFIs excluding the Eurosystem (see Chart C).

Chart C

Euro area portfolio debt securities transactions by main institutional sector

(four-quarter moving sums, percentages of GDP)

Sources: ECB and Eurostat.

Notes: For assets, a positive (negative) number indicates net purchases (sales) of non-euro area instruments by euro area investors. For liabilities, a positive (negative) number indicates net purchases (sales) of euro area instruments by non-euro area investors. The latest observation is for the fourth quarter of 2018.

As regards portfolio investment in the euro area, persistent net sales of euro area government debt securities by non-residents have been another key feature of euro area financial flows since the launch of the APP. This mainly reflects the important role of non-residents as counterparties to the Eurosystem in the implementation of the APP.[5] In line with this, non-resident investors’ net sales of euro area government bonds were particularly high in the four quarters up to the first quarter of 2017 (Chart C), i.e. in the period when average Eurosystem monthly net asset purchases peaked at €80 billion. Subsequently, non-residents’ net sales of euro area government debt securities gradually declined. In all likelihood, this fall was related to the stepwise reduction in the pace of Eurosystem net purchases until the end of 2018.[6] Non-euro area investors were also net sellers of euro area debt securities issued by financial corporations other than MFIs in 2018, while they became net buyers of debt securities issued by MFIs excluding the Eurosystem (see Chart C).

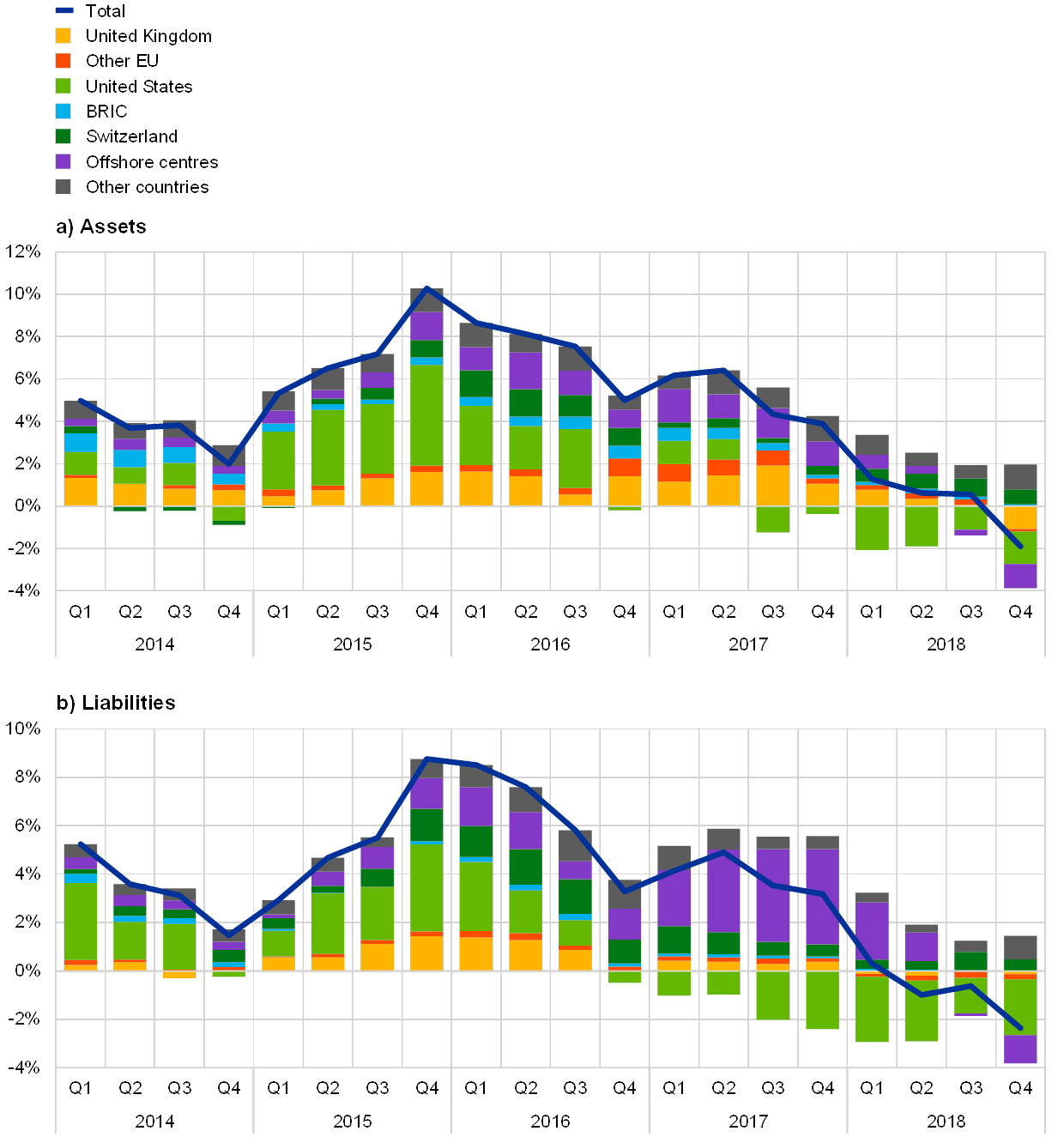

The retrenchment in FDI in 2018 mainly reflected transactions vis-à-vis the United States, linked in part to the US tax reform (see Chart D). The net FDI disinvestment in the euro area by US residents amounted to 2.3% of euro area GDP in 2018 and was particularly pronounced in the first half of 2018. This development is at least partly attributable to the impact of the Tax Cuts and Jobs Act passed by the US Federal Government in December 2017, which led to the repatriation of accumulated foreign earnings by US-based parent companies of multinational enterprises.[7] In addition, residents of offshore financial centres accounted for net FDI disinvestments in the euro area of 1.2% of euro area GDP, possibly also due to the impact of the US tax reform via intermediary entities resident in these jurisdictions. Moreover, this may also reflect changes to international tax policies aimed at addressing profit shifting practices of multinational enterprises. The largest net FDI investments in the euro area (0.5% of euro area GDP), on the other hand, were made by residents of Switzerland in 2018. Regarding euro area FDI abroad, euro area residents disinvested mainly from the United States (1.5% of euro area GDP) and offshore financial centres (1.1% of euro area GDP). The aforementioned US tax reform may also have been a factor in these cases, as multinational enterprises frequently channel their internal financial transactions via special purpose entities, some of which are resident in the euro area.[8] Moreover, for the first time since 2008, euro area residents made FDI disinvestments in the United Kingdom (1.1% of GDP) in 2018.

Chart D

Euro area foreign direct investment transactions by geographical counterparty

(four-quarter moving sums, percentages of GDP)

Sources: ECB and Eurostat.

Notes: For assets, a positive (negative) number indicates net purchases (sales) of non-euro area instruments by euro area investors. For liabilities, a positive (negative) number indicates net purchases (sales) of euro area instruments by non-euro area investors. “Other EU” comprises EU Member States and EU institutions outside the euro area, excluding the United Kingdom. The “BRIC” countries are Brazil, Russia, India and China. “Other countries” includes all countries and country groups not listed in the table as well as unallocated positions. The latest observation is for the fourth quarter of 2018.

- Other investment was relatively stable, as asset and liability flows increased to 2.0% and 2.7% of GDP respectively (from 1.9% and 2.1% of GDP in 2017).

- According to the dataset compiled in McQuade, P. and Schmitz, M., “America First? A US-centric view of global capital flows”, Working Paper Series, No 2238, ECB, February 2019.

- Between 9 March 2015 and 19 December 2018, the Eurosystem conducted net purchases of public sector securities under the public sector purchase programme, part of the expanded APP. See the ECB’s website for further details.

- See Cœuré, B. “The international dimension of the ECB’s asset purchase programme”, speech given at the Foreign Exchange Contact Group meeting, 11 July 2017, and Bergant, K., Fidora, M. and Schmitz, M., “International capital flows at the security level – evidence from the ECB’s asset purchase programme”, ECMI Working Papers, No 7, Centre for European Policy Studies, 2018.

- See the box entitled “Which sectors sold the government securities purchased by the Eurosystem?”, Economic Bulletin, Issue 4, ECB, 2017.

- See Cœuré, B., “The international dimension of the ECB’s asset purchase programme: an update”, speech at a conference on “Exiting Unconventional Monetary Policies”, organised by the Euro 50 Group, the CF40 forum and CIGI, Paris, 26 October 2018.

- “See FDI in Figures”, OECD, April 2019, and Emter, L., Kennedy, B. and McQuade, P., “US profit repatriations and Ireland’s Balance of Payments statistics”, Quarterly Bulletin, Central Bank of Ireland,- April 2019.

- “FDI in Figures”, OECD, April 2019.